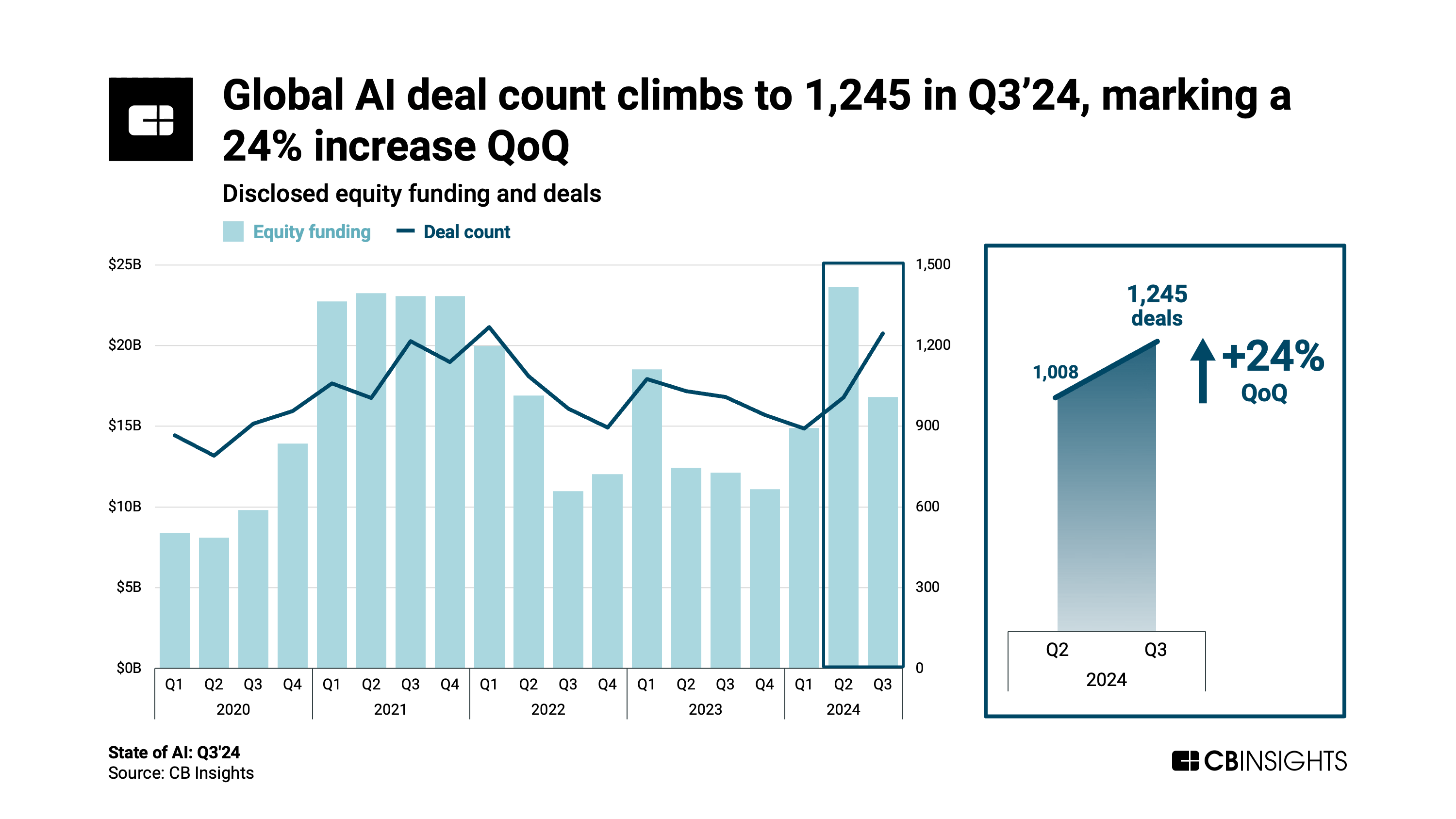

Quarterly AI deal count spikes to reach highest level since Q1’22 peak.

In Q3’24, global AI deal count skyrocketed 24% QoQ to reach 1,245 — its highest quarterly level since peaking in Q1’22. This contrasted sharply with activity in the broader venture sphere, where deal count fell by 10% QoQ to hit its lowest level since 2016/2017.

While AI deals in Q3’24 included massive $1B+ rounds to defense tech provider Anduril and AI lab Safe Superintelligence, global AI funding actually dropped by 29% QoQ. This was driven by a 77% decline in funding from $1B+ AI rounds QoQ.

Based on our deep dive in the full report, here is the TL;DR on the state of AI:

- Global AI deal count climbs 24% QoQ to reach 1,245 — its highest quarterly level since peaking in Q1’22. This bucked the trend in overall venture deals (-10% QoQ), signaling that investor interest in AI remains strong despite the broader cooling in venture markets. AI funding, on the other hand, fell by 29% QoQ to $16.8B, driven by a 77% decline in funding from $1B+ AI rounds QoQ.

- The average AI deal size is $23.5M in 2024 so far — up 28% vs. $18.4M in full-year 2023. This upward trend has been influenced by a rise in massive $1B+ deals, with AI startups drawing 9 of these deals in 2024 so far vs. 4 in full-year 2023. Top $1B+ rounds in 2024 YTD include:

These deals aren’t solely responsible for pushing up the average — the median AI deal size is up 9% in 2024 so far.

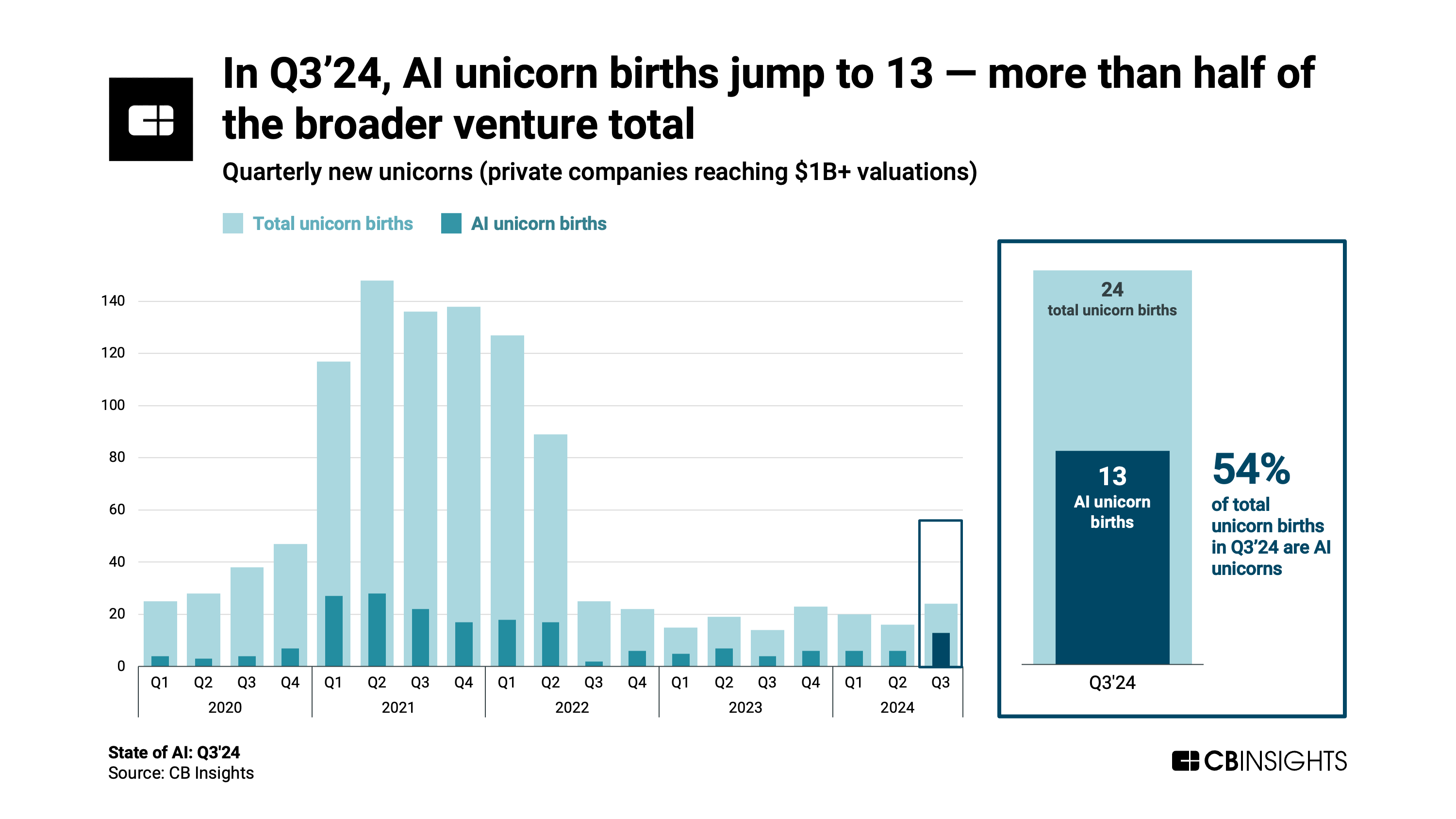

- AI unicorn births more than double QoQ to reach 13 — 54% of the broader venture total in Q3’24. Generative AI continues to be a key theme for new unicorns (private companies reaching $1B+ valuations). More than half of the AI unicorns born in Q3’24 are genAI startups, and they are working across a variety of areas — including AI for 3D environments (World Labs), code generation (Codeium), and legal workflow automation (Harvey).

Among new genAI unicorns in Q3’24, Safe Superintelligence — co-founded by OpenAI co-founder Ilya Sutskever — landed the most sizable valuation. The AI lab was valued at $5B after raising a $1B Series A round in September 2024.

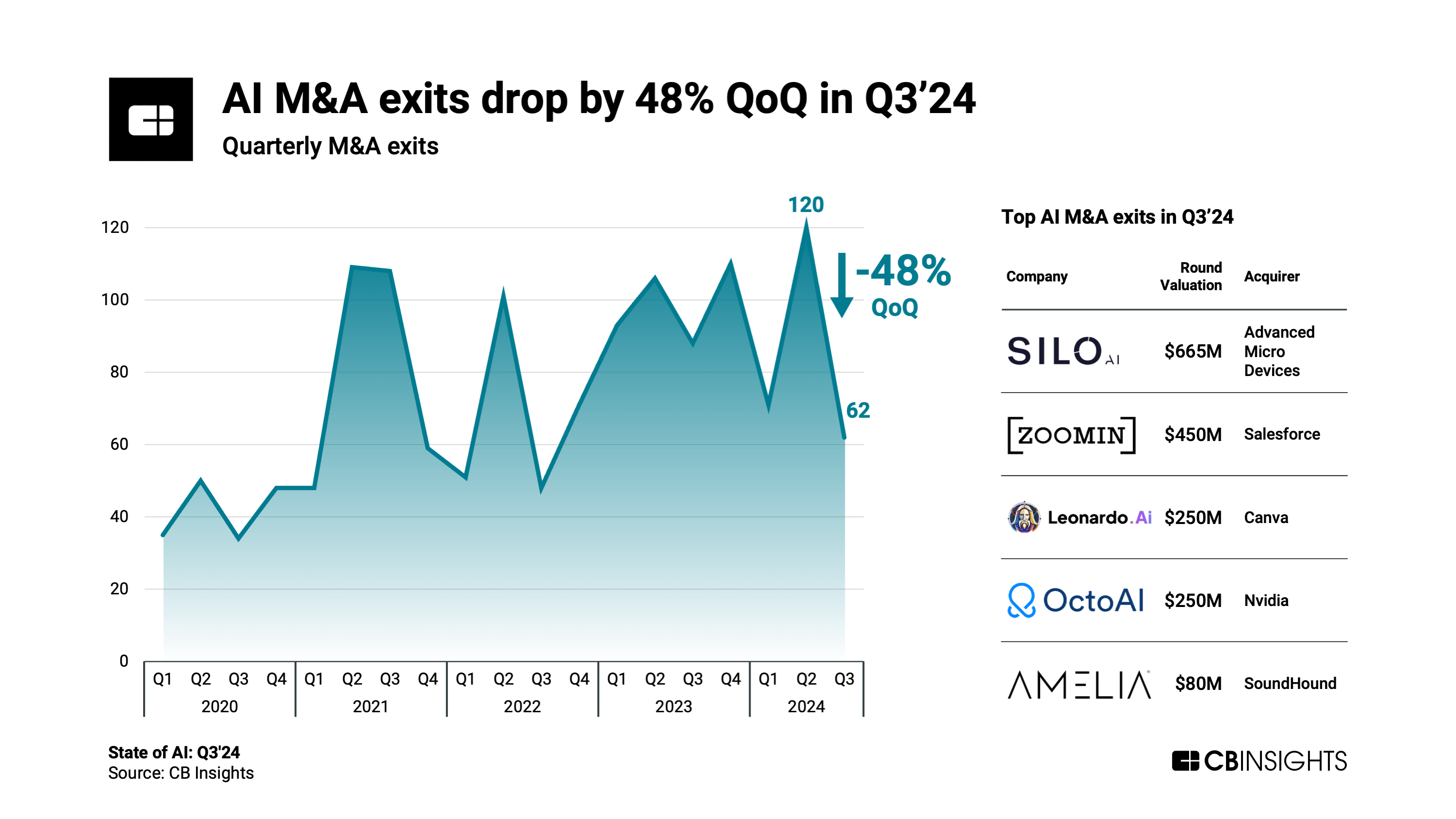

- AI M&A exits fall by 48% QoQ to hit 62 in Q3’24. The deals that did occur showcase how enterprises are strategically scooping up AI startups to improve their offerings and maintain a competitive edge. For example, the largest AI M&A deal in Q3’24 was AMD’s acquisition of AI lab Silo AI, which could help the semiconductor company enhance the development and deployment of AI models on its hardware. Meanwhile, Salesforce picked up unstructured data management startup Zoomin to support its AI agent offerings.

- Among major global regions, the US continues to lead in AI funding and deals. AI startups based in the US drew $11.4B across 566 deals in Q3’24, accounting for over two-thirds of global AI funding and 45% of global AI deals. Within the US, Silicon Valley still dominates AI funding and deals, but other metros are gaining ground. In Q3’24, Los Angeles and New York saw their AI deal counts rise QoQ while Silicon Valley watched its count drop for the second quarter straight.

ADDITIONAL AI RESEARCH FROM CB INSIGHTS:

- State of AI Q2’24 Report

- State of Venture Q3’24 Report

- Game Changers 2025: 9 technologies that will change the world

- The Multi-Agent AI Outlook: Here’s what you need to know about the next major development in genAI

- Analyzing a16z’s AI investment strategy: Where the firm sees opportunity amid the genAI rush

- The AI computing hardware market map